Get to know MESP

How Our 529 Plan Works

No matter your child’s age, the best time to open an MESP account is “today.” Because the sooner you start, the more you can take advantage of compound earnings and unique tax benefits.

Start early to make the most of your savings

Saving early has the potential to deliver compounding earnings over a longer period of time.

529 fact

529 fact

Help grow your savings with gifts from friends and family using Ugift®.

Advantages of Starting Early

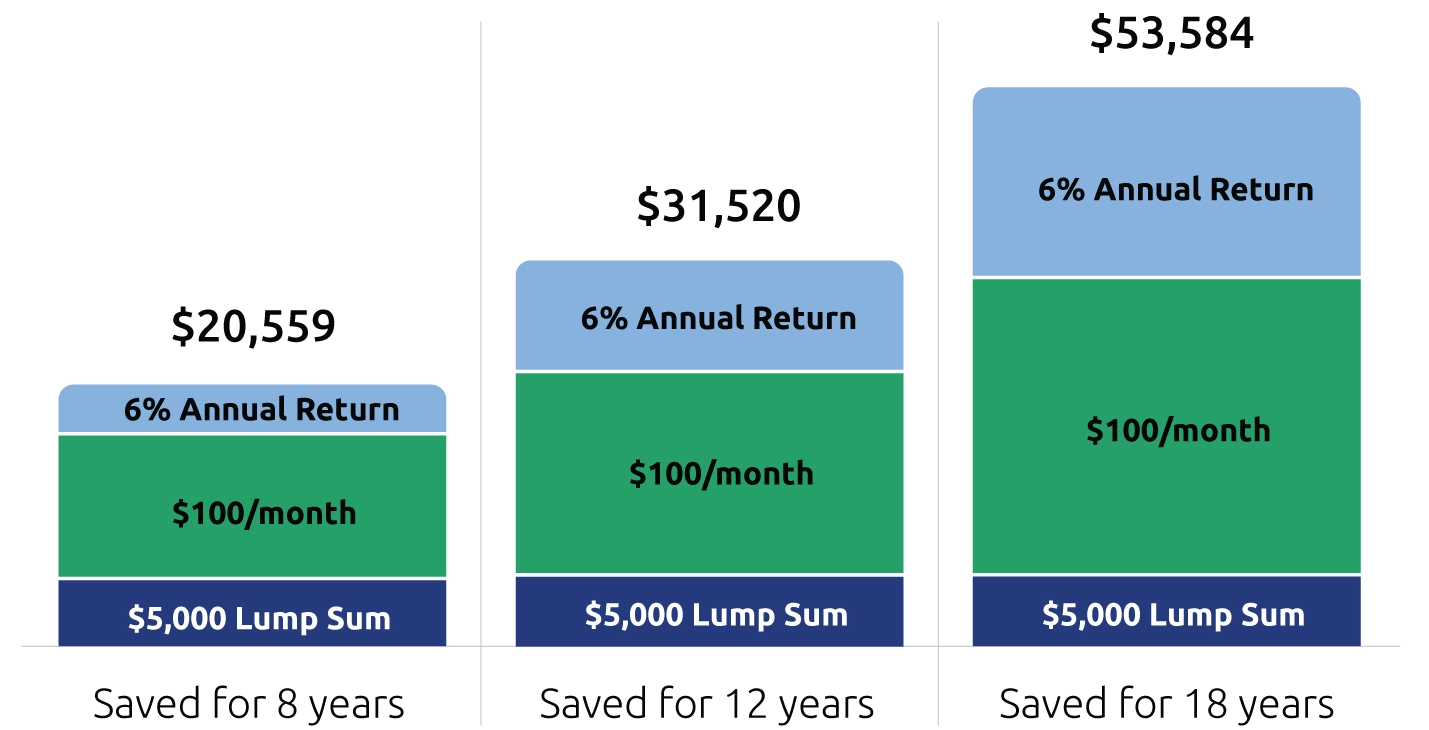

See how your savings might have grown if you started with $5,000 and continued to save $100 a month for 8, 12 and 18 years.

- Earnings

- Subsequent Contributions

- Initial Contribution

Save for 8 years

- Earnings: 6% Annual Return

- Subsequent Contributions: $100 per month

- Initial Contribution: $5,000 Lump Sum

- Total savings growth over time: $20,559

Save for 12 years

- Earnings: 6% Annual Return

- Subsequent Contributions: $100 per month

- Initial Contribution: $5,000 Lump Sum

- Total savings growth over time: $31,520

Save for 18 years

- Earnings: 6% Annual Return

- Subsequent Contributions: $100 per month

- Initial Contribution: $5,000 Lump Sum

- Total savings growth over time: $53,584

Graph Footnotes

- This chart assumes a $5,000 lump sum investment, a $100 monthly investment and 6% annual rate of return. The calculations are for illustrative purposes only, and the results are not indicative of the performance of any investments. The calculations do not reflect any plan fees or charges that may apply. If such fees or charges were taken into account, returns would have been lower. With any long-term investment, investment return may vary. Such automatic investment plans do not assure a profit or protect against losses in declining markets. Account value in the investment options is not guaranteed and will fluctuate with market conditions.

How much should you save towards your child’s tuition?

Get a quick estimate of approximately how much you’ll need to save using our calculator tool.

Estimate your savings

Unique tax benefits

When you pay fewer taxes, you can potentially earn more and grow your account faster—giving your child or grandchild an even bigger head start. MESP offers compelling income tax benefits.

- Individual taxpayers may deduct up to $5,000 in MESP contributions each year from their Michigan adjusted gross income, and taxpayers filing jointly may deduct up to $10,000.

- Investment earnings are 100% free from federal and state taxes when used for qualified education expenses.1

See the MESP Program Description for more details on our unique tax benefits.

WHO’S ELIGIBLE?

You, your friends, family, neighbors, and more…basically any citizen or taxpayer over 18 can open or contribute to MESP. Here are the details.

Account owners

- At least 18 years old with a valid Social Security Number (SSN) or Taxpayer ID Number

- Person opening the account can designate a successor account owner in the event of their death

- Certain trusts, estates, and corporations can also open an account with a valid taxpayer ID number*

Account Owner Footnote

- *Additional restrictions may apply; please refer to the Program Description for details.↩

Beneficiaries

- The beneficiary is the student and only needs a valid SSN or taxpayer ID number

- It can be your child, grandchild, even you—and you don’t need to be related to the beneficiary

- Only one beneficiary to an account, except when an entity creates a general scholarship account

Contributors

- Anyone can help pay for college with our easy and secure Ugift® platform

- Gifting may also provide advantages for estate and legacy planning; please consult your tax advisor2

An account can be opened in anyone’s name (like a parent, grandparent, or family friend) and easily transferred later.

Qualifying Expenses

With MESP, you have full control over how to use your funds. Here are the wide variety of qualified education expenses that can support your child in any path they choose to take:

- Tuition at any accredited private or public college or university, community college, trade school, graduate schools, and professional schools across the US and many abroad

- Certain room and board related expenses

- Fees, books, supplies and other equipment needed for enrollment and attendance

- Computers and related technology such as internet access fees, software or printers

- Certain additional enrollment and attendance costs for beneficiaries with special needs

- Pay for K-12 qualified expenses at a public, private or religious elementary, middle or high school - up to $20,000 annually federal tax free3

- Pay for apprenticeship expenses Federal Tax free—Apprenticeship programs must be registered and certified with the Secretary of Labor under the National Apprenticeship Act.3

- Pay for qualified expenses when enrolled in a recognized postsecondary credentialing program4

Funds can also be used in two other helpful ways:

- Repay student loans—up to a $10,000 lifetime limit per individual (including principal and interest on any qualified education loan)3

- Transfer additional/leftover funds to another eligible beneficiary such as another child, grandchild, or even yourself

Please see the state tax treatment of withdrawals section in the Program Description for more information.

See plan details for additional information

Have more questions?

No. Your MESP funds can be used at any accredited university in the country—and even some abroad. This includes public and private colleges and universities, apprenticeships, community colleges, graduate schools and professional schools.1 Up to $20,000 annually can be used toward K-12 qualified expenses.1 In addition, your 529 can be used for student loan repayment up to $10,000 lifetime limit per individual.1 Review a list of qualifying expenses and the state tax treatment of withdrawals for these expenses in the Program Description.

Footnotes

- 1Withdrawals for tuition expenses at a public, private or religious elementary, middle, or high school, can be withdrawn free from federal taxes. For Michigan taxpayers, these withdrawals are subject to recapture of Michigan income tax deduction and state income tax on the earnings. Registered apprenticeship programs and student loan repayment can be withdrawn free from federal and Michigan income tax. You should talk to a qualified professional about how tax provisions affect your circumstances.↩

With your MESP account, you're never locked in. You'll always have access to several options for this money:

- Your funds can be used to pay for a variety of eligible education expenses, including at any accredited college, university, apprenticeships, community college or postgraduate program in the United States—and even some schools abroad.1

- Your 529 can be used for student loan repayment up to $10,000 lifetime limit per individual.1

- Pay for K-12 qualified expenses - up to $20,000 annually can be used per student at a public, private, or religious elementary, middle, or high school. Qualified education expenses include curriculum, instructional materials, tutoring by approved professionals, standardized test and dual enrollment fees, and licensed educational therapies for students with disabilities.1

- You can transfer the funds to another eligible beneficiary, such as another child, a grandchild or yourself.

- If you just want the money back, you can withdraw the funds at any time. If funds are withdrawn for a purpose other than qualified higher education expenses, the earnings portion of the withdrawal is subject to federal and state taxes plus a 10% additional federal tax on earnings (known as the “Additional Tax”). See the Program Description for more information and exceptions.

- Pay for qualified expenses when enrolled in a recognized postsecondary credentialing program.2

-

Effective January 1, 2024, 529 funds may be rolled over to a Roth IRA in the name of the beneficiary of the 529 Plan.

State tax treatment of a rollover from a 529 plan into a Roth IRA is determined by the state where you file state income tax. There are conditions that must be met including the 529 Plan must have been in existence for at least 15 years.

You should talk to a qualified professional about how tax provisions affect your circumstances.

Funds rolled over to a Roth IRA can be withdrawn free from federal taxes. For Michigan taxpayers, pending a determination by Michigan authorities it is unclear whether a rollover from a 529 plan account to a Roth IRA by Michigan taxpayers will be treated as a non-qualified rollover and subject to Michigan state tax income tax and Michigan's deduction recapture provisions. Account Owners and Beneficiaries should consult with a qualified tax professional before rolling over funds from their 529 plan to contribute to a Roth IRA.

Footnotes

- 1Withdrawals for tuition expenses at a public, private or religious elementary, middle, or high school, can be withdrawn free from federal taxes. For Michigan taxpayers, these withdrawals are subject to recapture of Michigan income tax deduction and state income tax on the earnings. Registered apprenticeship programs and student loan repayment can be withdrawn free from federal and Michigan income tax. You should talk to a qualified professional about how tax provisions affect your circumstances.↩

- 2Withdrawals for Recognized Postsecondary Credentialing Programs—including tuition, books, equipment, supplies for the enrollment or attendance, testing fees if required to obtain or maintain a Recognized Postsecondary Credential, fees for continuing education if required to maintain an RP Credential and therapies for students with disabilities—are exempt from federal income tax. For Michigan taxpayers, pending a determination by the Michigan authorities it is unclear whether Postsecondary credentialing and Continuing Education will be treated as a non-qualified withdrawal and subject to Michigan state income tax and Michigan deduction recapture provisions. Consult a tax professional for guidance.↩

Your MESP account can be used at eligible colleges, universities, vocational schools, community colleges, graduate or postgraduate programs, apprenticeships, credentialing programs and more.1 Contact your school to determine whether it qualifies as an eligible educational institution or use the Federal School Code Search tool on the Free Application for Federal Student Aid (FAFSA) website.

Footnotes

- 1Registered apprenticeship programs and student loan repayment can be withdrawn free from federal and Michigan income tax. You should talk to a qualified professional about how tax provisions affect your circumstances.↩

There are no sales charges, startup fees or maintenance fees associated with MESP accounts. For details on total annual asset-based fees, comprised of the underlying investment expenses for each investment option, the program manager fee and state administration fee, review the individual investment options Fee Table in the Program Description.